Digital Envelope Budgeting: An Old-Fashioned Budgeting Method for Modern Times

Budgeting is an integral part of simple living. Simple living is all about being intentional. How we spend our money is a direct reflection of our values. If we aren’t being intentional with our spending, if we are frittering money away without knowing where it is going, then we don’t truly value it. Since money is a result of energy exchange (we are generally trading our time for money), it’s important to be mindful of our spending, so we are also being intentional about our time. We buy things not with dollars, but with hours of our lives. However, learning to budget can feel complicated. I love to use envelope budgeting, but cash envelopes were just not practical. I have embraced digital envelope budgeting, a simple, old-fashioned method of budgeting, but adapted for our modern times.

Why do we need to budget?

How often do you feel like there isn’t enough money to go around?

Do you find yourself spending carelessly, only to later remember that an annual or quarterly bill is due, that you completely forgot about?

Do you budget based on your bank balance, and then run out of money before the month is over?

Are you living paycheque to paycheque? Meaning you drain your bank account balance to almost nothing, then have to await your next paycheque to arrive so you have more money?

Do you have money set aside for emergencies? How about home repairs and car repairs? What about when it’s time to replace your vehicle? Will you need to resort to a car payment, or have you planned ahead and set money aside?

Do you dream about a vacation, but the only way you could take one would be if you put it on your credit cards?

Speaking of credit cards – do you carry a credit card balance? Or perhaps have multiple credit cards with balances?

I used to feel so overwhelmed when it came to budgeting

When you’re young and single, budgeting is simple. You might have rent to pay, maybe basic utilities like internet and cell phone – you don’t have to think too much about whether you have enough money set aside for multiple things.

Once you have a family, a home, vehicles, etc. – budgeting becomes a little more complex. You can no longer rely on your bank balance as an accurate way to determine if you have enough money to cover your expenses. We have way more expenses, and it’s simply impossible to keep track of it all in your head.

Routine annual expenses can catch you off guard – and you start treating them like emergencies. (Hint: Christmas comes on the same day each year).

I knew I needed to up my budgeting game, in order to ensure that all of our expenses were covered – even those ‘surprise’ annual ones.

The Old Fashioned Envelope Method

Back in the day, people used to literally divide their (cash) paycheques into various envelopes. There would be an envelope for their house payment, one for groceries, maybe another one for gas. There would be an envelope for clothing, and perhaps one for home repairs.

This way, instead of seeing your paycheque as a lump of money that is available for spending, you would divide it into the envelopes, and instantly have a reality check about how much money you actually have. Perhaps 1/2 of each house payment would come out of each cheque and go into the envelope. Then the rest would get divided among other needs.

I’ve even heard of people having a ‘Christmas Club’ bank account, where they would squirrel away a little from each paycheque, so they would have enough money come Christmas, without having to sacrifice their bills that month.

The point is, envelope budgeting was a simple, smart, tangible method of managing your finances.

Once the envelope was out of money, you were done spending for that month. Unless you borrowed from another envelope. But if you did, you would be leaving yourself short in that other category (it’s probably not smart to borrow from your house payment envelope).

This worked beautifully when people primarily used cash for all of their transactions.

Cash is a beautiful method of payment. They have literally done studies, showing the pain centre of your brain lights up when you hand over cold, hard cash for something. The same effect did not take place when using plastic (whether it was debit or credit made little difference).

Cash is real, it’s tangible, you have to count it, which means you pay attention to the amount (how often do you hand over your debit card without even realizing how much the transaction total was?)

I LOVE using cash for spending.

Cash is King, but it’s not practical

However, using cash for every transaction is just not realistic.

You can’t use cash when you order something online.

Most banks won’t let you make your mortgage payment in cash.

You CAN pay your bills in cash, but it would require a physical trip to each utility provider in order to make the payment (most of us aren’t willing to do that).

With inflation, we would need to carry around a LOT of cash in order to cover all our expenses for the week or month.

If you have a spouse/partner and are sharing finances, it gets even trickier. What if the grocery envelope is at home, but your asked your partner to stop and pick up something at the grocery store on their way home? Who keeps the envelopes?

The Envelope Method for a Digital World

I LOVED the concept of the envelope method; the idea of parceling out every dollar to a category (also known as a Zero-Based Budget – where you spend all of your dollars on paper until you reach a balance of 0).

However, using real paper envelopes was just not practical.

I have also found that I tend to stay more organized using digital methods (see my post about how going digital simplified my life). So my ideal solution was an app that used the same principles as envelope budgeting, but was a better fit for our modern world.

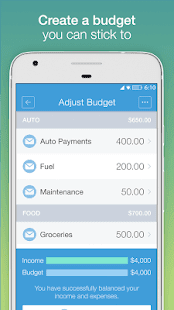

I found an application called Mvelopes. Basically, it was exactly what I wanted – it allows me to divide our funds up into virtual ‘envelopes’, and I can take the app with me on the go, to enter transactions as I spend.

My husband also has the app, and also enters his own transactions – so we both stay aware of how much is left for spending in each category, and we know to slow down when the envelope is getting close to empty.

Budget Categories/Envelopes

One of my favourite features of Mvelopes, is it allows you to group envelopes together in various categories. So basically, you can have categories and sub-categories.

Here is an example how we have our envelopes categorized:

- Monthly Bills (recurring monthly expenses)

- Mortgage

- Hydro (electricity)

- Insurance

- Cellular

- Netflix

- Internet

- Periodic Bills (recurring bills that come less frequently than monthly)

- Amazon Prime (annual)

- Auto registration (annual – plate renewal)

- CAA (annual)

- Evernote (an app we use for homeschooling – annual renewal)

- Property tax (paid 2x/year)

- Expenses (day to day living expenses/spending)

- Allowance (each family member gets a small amount of spending $ each month)

- Fuel/parking

- Auto maintenance

- Auto replacement

- Christmas

- Clothing & footwear

- Date night

- Family fun

- Groceries

- Meat (we buy meat in bulk 2-3x/year, so we save separately for this)

- Gardening

- Gifts & occasions (everything but Christmas)

- Health (non-insured health-related expenses)

- Personal care (hair cuts, etc)

- Propane (we heat with propane, plus use it for our bbq)

- Skye (or dog has her own budget – anything relating to pet care, including dog food, comes out of this)

- Vacation (this fund currently sits at zero, but hey, we can dream!)

- Savings

- Emergency Fund

Benefits of Envelope Budgeting

There are SO many benefits to envelope budgeting, that I couldn’t imagine budgeting any other way.

Most ‘budgeting’ programs are actually spending trackers. They help you figure out where your money went AFTER you spent it.

That’s not budgeting.

Other programs teach you to guess at what you’d spend in a category, but without actually putting money IN that category, there is no accountability. You’re just spending and hoping to stay within what you guessed you would spend.

With Mvelopes, it’s real, it’s tangible. You see the balance diminishing as you spend out of the ‘envelope’.

It forces you to realize you have less money than you think you do.

How many people get excited for pay day, because they suddenly think they have all this money to spend? But then their car insurance comes due, or they need new tires, or they get their property tax bill in the mail, and think – crap, I should have set some of that aside.

It keeps you out of debt.

Debt is simply spending that you didn’t plan for.

So many people only consider their monthly expenses, and don’t think ahead to their periodic or annual expenses.

This is usually when the credit cards come out. Instead of saving ahead for these expenses, they are now considered emergencies – and this starts the slippery slope into debt. Our family chooses to live debt-free, so we truly have no choice but to save up for these expenses – because going into debt simply isn’t an option for us.

It helps you create a true emergency fund.

So many people try to save an emergency fund, but it gets depleted every time they have a car repair or a home repair – because they consider those to be emergencies.Car repairs and home repairs are NOT emergencies! If you own a home or a vehicle, maintenance costs should be factored into your budget. The cost of owning a vehicle isn’t just the insurance and the gas.

Maintenance and repairs are inevitable. BUT they tend to be periodic – so figure out approximately what you will spend per year on maintenance, divide it by 12, and set that aside in your monthly budget.

I can’t tell you how comforting it is when a car repair needs to be done, and we have a little cushion built up in our car maintenance fund. It turns a stressful situation into something we don’t need to stress about!To me, an Emergency Fund should be reserved for TRUE emergencies. ie) job loss, an unanticipated health emergency, or something catastrophic. Pretty much everything else, we can anticipate!

It makes you look for good deals.

If you budget based on your bank balance, you tend to think you have more money than you actually do. You don’t work as hard to try to find deals, because there appears to be an infinite pile of money that just replenishes itself every time you get paid. (Until, of course, something comes up!).

When you break that pile up into envelopes, you see that you actually just have a bunch of tiny piles of money. Depending on your budget, those tiny piles likely won’t stretch very far.

You have to live within your means. That means you are realistic about your grocery budget, and find ways to eat healthy for less money.

You do home repairs yourself, because buying the materials is cheaper than paying for labour, and you know that you don’t want to spend every cent in your home maintenance budget, because there will always be something that needs doing.

You buy things second hand, because you realize that your clothing budget, for example, has to cover 5 people, and that includes boots, winter coats, and all clothing – so you stretch that budget by thrifting, passing down items between kids, and patching knees to make things last just a little longer.

It doesn’t matter what form of payment you use.

With digital budgeting like Mvelopes, the app doesn’t care what form of payment you use.

Whether it’s a credit card, cash, your debit card, an e-transfer, etc. – it all gets subtracted out of the envelope.

This is especially helpful for those who like to use credit cards for payment. We tend to be surprised when the credit card bill arrives – what the heck did we spend all that money on?

With Mvelopes, the amount gets subtracted from the envelope no matter what form of payment you use. And if you use a credit card, it automatically moves that amount to the ‘for credit card’ envelope.

What that means, is when the bill arrives, that money is already accounted for in your budget. All you do is pay the bill! No surprises, and no spending the same money twice.

Our family only uses credit cards for online shopping, and we use cash and debit for everything else. But even online shopping can get away from you if you don’t keep track. So I love the feature of having it set aside into the credit card envelope so we can just pay it when it comes in.

The downside of traditional cash envelopes is if you use your debit card or credit card, it messes up your whole budget! This way, every cent is accounted for, regardless of how you choose to pay.

It allows you to dream

As you can see, we have a ‘Vacation’ envelope, that currently has $0 in it. But you know what? The fact that that envelope is there, reminds us that we have a goal of traveling. We can choose to cut back on other expenses if we wish, and funnel some money into the Vacation fund. Or we can have a yard sale, or come up with creative ways to earn extra money to fill up that envelope.

Are there other good envelope budgeting apps?

Disclaimer: I have been using Mvelopes for well over a decade. It has served me extremely well, and save for a few glitches here and there, I highly recommend it.

I sometimes become curious, and want to see what else is out there, so I have tried a few different programs, but ALWAYS end up back with Mvelopes.

I actually bought it way back when they had a Lifetime membership option – after using it for free for many years, they introduced a fee. I could either choose to pay monthly, or buy the lifetime membership and never have to pay again. Since it was SUCH a valuable tool for my family, I chose to purchase the lifetime membership.

This is no longer an option, but they do have a 30-day free trial, and then 3 monthly subscription tiers after that.

Get your 30-Day Free Mvelopes Trial HERE.

With all that said, here are a few other apps that work in a similar way, but I can’t vouch for them, because I don’t use them myself.

YNAB (You Need a Budget)

Everydollar (Dave Ramsey’s envelope budgeting software)

Do you use the envelope method for budgeting? Do you use real cash and envelopes, or digital?

PIN IT FOR LATER!